Personal Finance 101: Manage Your Money Wisely

You do not need to be a financial expert or have a finance degree to be good at managing your money. Anyone can have good personal finance strategies in place if they take the time to educate themselves on the topic.

I've read many personal finance books over the past few years and listened to even more podcasts outlining how to become financially independent. By implementing the strategies I learned over the years, I was able to automate my financial life.

I learned to focus less on managing my money once I had a system in place, so I could focus on the things that matter.

What is personal finance?

If you ask me, personal finance is the art of automating your financial life. When you do not have to worry about budgeting, savings, investing, debt, or retirement because your money is already going to those places before you even start spending.

Unfortunately, we are not born financially savvy and many of us did not learn about personal finance in school. It is up to us to become financially literate so we can meet our financial goals.

Use this guide as a foundation to better your understanding of personal finance and money-making decisions so you can increase your net worth.

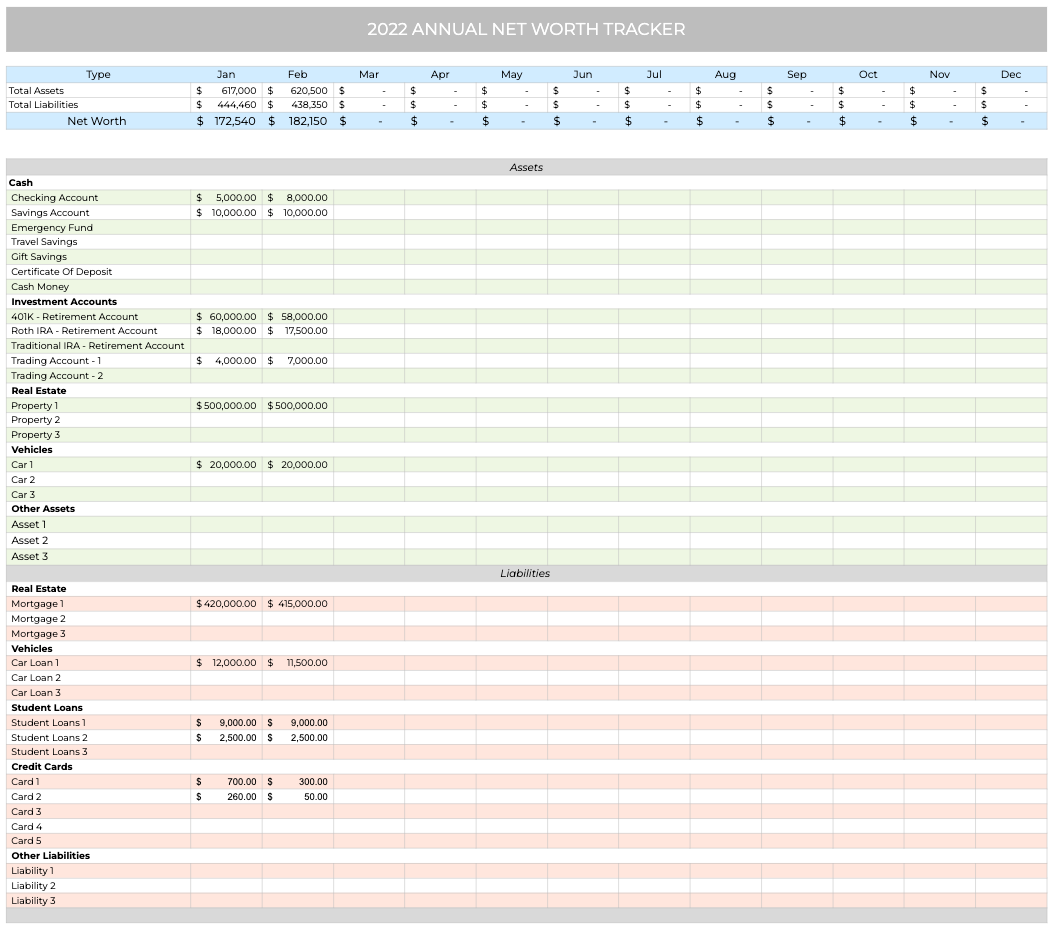

Annual Net Worth Tracker Template

A simple and sleek way to track your annual net worth to stay on track to meet your yearly financial goals.

1. Getting Out of Debt / Avoid Debt

Debt is the worst thing that anyone can be in, and I would not wish it on my worst enemy. Of course, there is good debt and bad debt, but for this purpose, let us agree that all debt is bad.

Credit cards, for instance, are one way many people fall into debt. It is so easy to swipe your card at the register, but when you cannot pay back all of your balance at the end of the month, you can get into debt very easily.

Student loans are another agonizing form of debt. You are fresh out of college and find yourself having to pay a few hundred dollars monthly to pay off thousands of dollars in debt just because you decided to get an education.

It is frustrating! That is why you should avoid borrowing money by all means if you can.

The important thing to know is that if you owe money, make more than the minimum payments. It is not worth it to pay all the fees and interest.

Pay off the debt with the highest interest rate first, regardless of the amount. That will allow you to finish paying faster. Getting out of debt is a critical first step toward beginning to save and invest for your future.

2. Budgeting

When you hear the word budget, it is often associated with limiting your spending. However, budgeting is just a tool to understand the money you bring in (income) and the money going out (expenses).

Creating a monthly budget sets you up for success because you determine where your money should go before it is spent. It allows you to figure out how much money you should allocate for savings and how much you can afford to spend on entertainment.

My favorite budgeting rule is the 50-30-20 rule. It states that you should allocate 50% of your income to essential spending, 30% to your needs, and 20% to your savings.

You should always allocate to savings first before expenses. That is what you call paying yourself first, a concept I learned from Rich Dad, Poor Dad by Robert Kiyosaki. It is a simple yet powerful concept that separates the rich from the poor.

Preferably, you should have a surplus on a monthly basis that you can then allocate to another financial goal. If you have a negative budget, your spending will outweigh your income, which essentially puts you in debt.

In that case, you will need to either cut down on your expenses or find a way to increase your income. For instance, getting a higher-paying job or starting a side hustle.

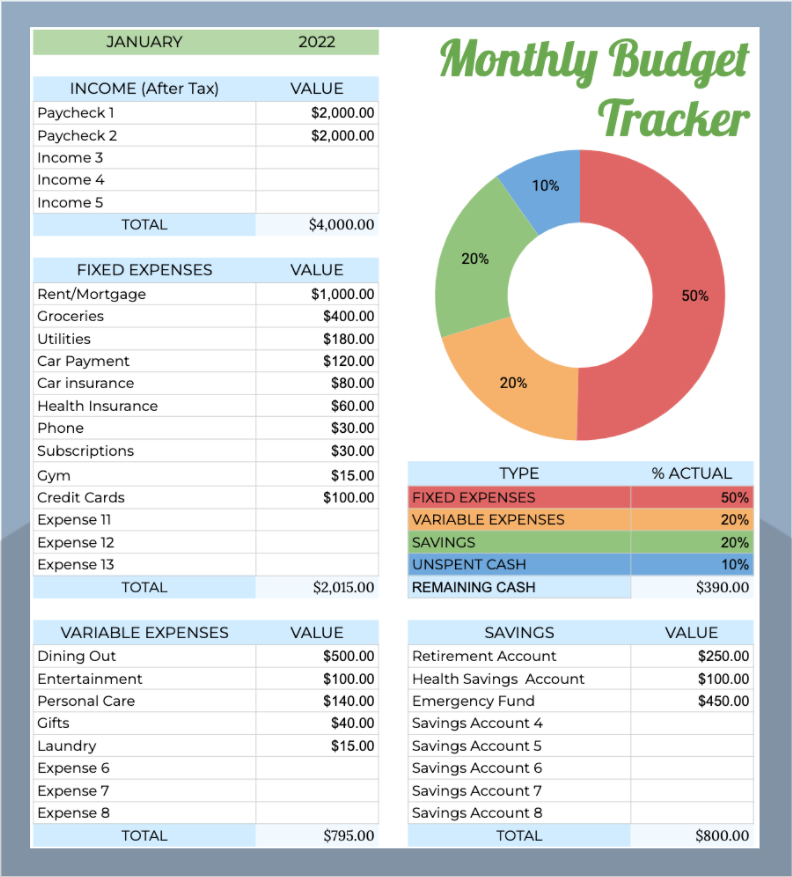

Monthly Budget Tracker Template

A simple tool to help you track your monthly spending and determine how much money to save and invest on a monthly basis.

3. Building an Emergency Fund

An emergency fund is exactly as it sounds, a safety cushion for emergencies. Let's say you got laid off at work, there was an unexpected medical bill not covered by insurance, or your car broke down.

Whatever the emergency, it was not covered in your monthly budget. You do not want to dip into your investments to cover such things, and that is the purpose of having an emergency fund.

Aim to build up your emergency fund to be 3-6 months of your monthly expenses. So if your monthly expenses are $2500, then your emergency fund should be $7500-$15000.

Keeping your emergency fund separate from your regular checking bank account will tame the temptation to use it.

4. Investing into Retirement

This is very important, and the earlier you start, the better. Start off by putting money into your company’s 401(k) plan or whichever plan they offer. Most companies offer a certain percentage match on how much you contribute.

Do not leave any money on the table, and make sure to contribute enough money to get that.

Ideally, you want to aim for 10–15% of your salary for retirement. If you started saving for retirement late (say in your 30s), maybe consider even saving 20% of your income. Experts recommend having 1.5 times your salary in retirement accounts when you are 30.

After you have your employer’s account in check, the next step is to invest money in a Roth IRA. It's a tax-advantaged account that allows you to save money on taxes when you retire. You can open a Roth IRA using M1 Finance.

5. Enjoy Life

Now that you have got the basics down, you do not have to worry about where your financial future is heading. You build a strong financial foundation, and you can start thinking about saving for a yearly vacation, a downpayment on a house, or even a fancy car.

The most important thing is to start taking action towards your finances immediately. The earlier you start, the more your future self will thank you.