401K vs Roth IRA: Retirement Investing

I often get the question, "Should I go with a 401(k) or a Roth IRA?"

Today we will discuss the differences between the two retirement accounts. There are advantages and disadvantages to both accounts, but we will discuss the best way to utilize both accounts.

Also, we will take a look at monetary examples of how your money will grow in each account over 30 years of consistent investing.

1. 401(k)

A 401(k) is a type of retirement investment account that is offered by your employer or workplace and has tax advantages. The key point here is that this is a retirement account, which means you will utilize the tax advantages if you do not withdraw until the age of 59 ½.

A benefit of having a 401(k) is that the money leaves your paycheck for your 401(k) before it gets deposited into your checking account.

A 401(k) account benefits from being a tax-deferred retirement account. This means that you contribute pre-tax dollars and you will pay taxes on your withdrawals in retirement. The 2022 contribution limit for employees is $20,500.

Essentially, you are contributing more money now to take advantage of compounding and will pay taxes in retirement when, hopefully, you are in a lower tax bracket.

Because this is a long-term retirement account, you will be penalized by 10% if you withdraw your money before reaching the age of 59 ½ years. In addition, you will be required to pay taxes on that withdrawal. You will also be forced to withdraw some of your money at age 70 ½.

2. 401(k) Tax Savings

Let's take a look at how contributing to your 401(k) saves you money on taxes in the short term. Personally, I’m in the 24% tax bracket.

By choosing to contribute the maximum contribution amount to my 401(k), I would be saving 24% on $20,500 in short-term taxes, which is $4,920. Remember, your 401(k) contributions are subtracted from your taxable income.

3. 401(k) Employer Match

The majority of employers provide an employee contribution match, meaning you get free money to invest in your retirement.

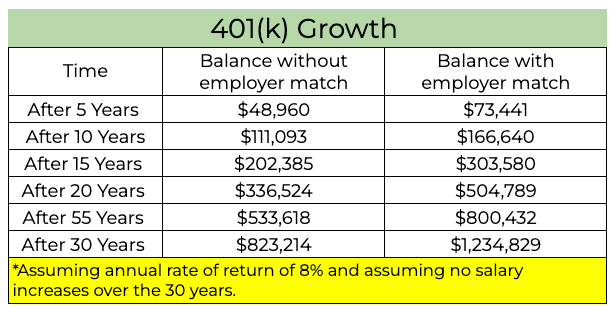

Let’s take a look at an example. Say you make $80,000 at your current job. Your employer offers a 50% match up to 8% of your salary. You need to contribute a minimum of 8% to maximize this benefit and not leave any money on the table. Your 8% contribution is $6,400, in addition to the $3,200 from your employer’s match. Now you have an initial investment of $9,600 in your 401(k).

Here is how that money will grow over the next 30 years for your retirement:

4. Roth IRA

A Roth IRA is another type of retirement investment account that is self-directed. This means that you control when you contribute and what funds or stocks should be in that investment account. The contribution limit in 2022 is $6,000 and $7,000 if you are 50 or older.

A Roth IRA differs from a 401(k) in its tax advantages. With a Roth IRA, you contribute after-tax dollars, but your money grows tax-free. Thus, when you withdraw money in retirement, you won't have to pay taxes as long as you are 59 ½ or older. This makes it advantageous even in contrast to a standard taxable account.

Because this is a long-term retirement account, you will be penalized by 10% if you withdraw your earnings before reaching the age of 59 ½ years. You can, however, withdraw your contributions after 5 years of account opening with no penalty.

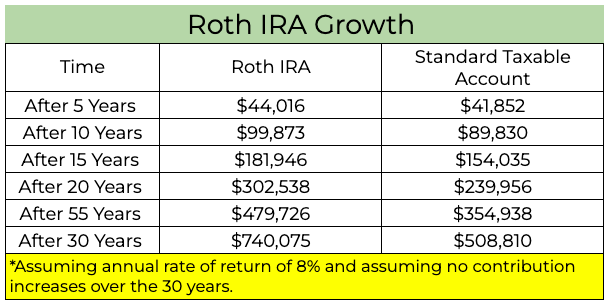

Here is how your Roth IRA will grow tax-free if you contribute $6,000 every year for 30 years:

5. Bottom Line

Both the 401(k) and the Roth IRA have favorable tax advantages. The good thing is that you can contribute to both at the same time.

If your employer offers a 401(k) match, take advantage and contribute enough money to get the company match. Once you maximize the company match, then I would max out the Roth IRA for the year. If you still have money left over for investing, I would then return to contributing to the 401(k) and maximize contributions in that account as well.

If your employer does not offer a 401(k) match, I would max out my Roth IRA first. Then I would start contributing to my 401(k) to reduce my taxable income and take advantage of the short-term tax benefits.